US Auto Repossessions Hit 16-Year High Amid Economic Strain

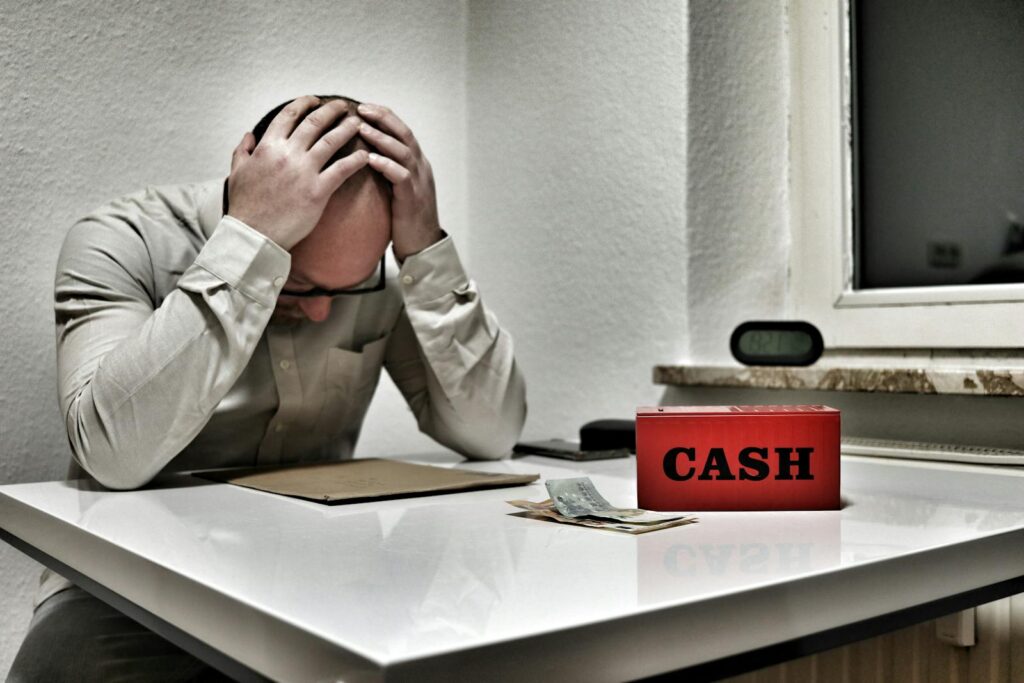

With the rise of auto repossessions in the United States, it has become one of the most obvious indicators of financial strain within American households. Once people were able to afford everything they needed every month, they’re now trying to pay all of those bills, mortgage payments, groceries, and utilities without breaking the bank. For most Americans, cars are no longer considered luxuries. They’re essential devices for work, school, medical appointments and daily life. The loss of a vehicle can have a profound impact on a person’s life, particularly in regions with a limited or unreliable public transit network.

The price of car ownership has risen significantly over the last few years. The price of new cars has risen significantly, the value of used cars has been volatile since the beginning of the pandemic and interest rates have climbed at a rate that many consumers have not expected. Meanwhile, inflation kept gradually eroding household budgets month by month. The news may be about stock market rallies and solid corporate profits, but many working families are experiencing a vastly different economy. For them, it’s a balancing act with finances and a bill that’s taking up more and more of the budget: auto loans.

New data now reveals that vehicle repossessions are now at their highest level over the past 16-plus years, and are reminiscent of the financial woes during the Great Recession. The current economy is not in the same mess as the one in 2008, but the surge in late payments and delinquencies is creating worry for economists, lenders and legislators. The situation taking place in parking lots, driveways and neighborhoods around America is just a symptom of a much bigger affordability problem in the economy that is simmering away quietly.

1. Auto Repossessions Rising Sharply

Cars being taken back by lenders have hit a high not witnessed since the economy crashed more than a decade ago. Across the country, millions of people find it harder each month to cover what they owe on their vehicles as money gets tighter. Data collected through 2024 shows repossession numbers jumped fast, signaling wider strain hitting households regardless of income level. Because getting around often means keeping a job or handling basic needs, many stretch budgets just to make car payments last. Even those working full time and paying other bills face breaking points defaults rising quickly reveal how thin margins have become.

Rising Repossessions and Financial Pressure:

- Record-high nationwide vehicle repossessions

- Borrowers struggling with rising expenses

- Defaults increasing beyond recession levels

- Transportation remaining financially essential

Lately, more cars are being taken back, showing just how tight money matters have gotten at home. When prices climb and loans grow heavier, even careful payers can slip into arrears. Without a car, life gets harder getting to work, school runs, errands all shake loose. Trouble keeping up payments isn’t rare anymore; it’s spreading through neighborhoods like a slow leak. Behind each repossessed vehicle sits a story of choices narrowed by cost.

When cars start piling up at auction lots, it is rarely just bad luck. People tend to keep making auto payments even after cutting back on everything else first. Trouble shows when that last priority becomes impossible too. What looked like steady income now reveals hidden cracks under pressure of rent, food, fuel. These returned vehicles stack higher each month quiet proof something deeper has shifted.

2. Car Costs Keep Rising

These days, buying a car feels much harder than it did just a few years back. Prices for brand-new models sit near record levels, making them out of reach for plenty of people. Even secondhand vehicles cost noticeably more compared to pre-pandemic times. Shortages in parts, limited factory output, along with steady buyer interest, kept pushing prices upward. Many ended up stuck choosing lengthy loan deals just to get behind the wheel. When getting around is essential, waiting usually wasn’t possible.

Rising Costs of Owning Vehicles:

- New car prices near records

- Used vehicles remain highly expensive

- Inflation increasing total ownership expenses

- Families forced into costly loans

Heavy bills pile up fast when car costs climb. On top of the payment, things like repairs, insurance, gas, and paperwork fees eat deeper into paychecks. Folks who bought cars when prices hit record highs are stuck handing over way more cash each month than planned. A small money problem like a doctor visit or leaky roof can make it tough to keep up with what they owe.

Heavy car prices mixed with growing everyday bills now stretch budgets thin for workers who need wheels. Some people signed loan deals when they felt rushed, leaving little room to manage money later on, say finance watchers. With spending demands piling up at home, buying a car weighs harder on household finances than it once did. Fewer dollars go further these days, making long-term payments feel tighter across the country.

3. High Interest Rates Strain Household Finances

These days, paying for a car feels heavier because of rising interest charges. People borrowing money might see rates jump into the teens, particularly if their credit record is thin or marked with setbacks. Because of steeper fees piling up each month, what seemed like a manageable price at first grows much larger over time. Instead of lowering what people owe right away, banks are stretching payback periods some go half a decade or longer just to shrink the bill due every few weeks.

Long Term Loan Money Problems Over Time:

- Rising interest rates increasing debt

- Extended loans reducing short-term payments

- Borrowers trapped in lengthy financing

- Monthly costs straining household budgets

Lent over years, a car payment might feel easier each month at first. Yet stuck owing long after the wheels stop turning well happens too much. As prices drop fast on used models, people find themselves trapped paying for something worth little. Money set aside for doctors, food, rent, or kids’ needs gets pulled toward auto bills instead. Balancing what matters becomes harder when so much rides on one vehicle’s clock running out.

Money advisors say rising loan rates are changing how people buy cars across the U.S. Still making ends meet? Not anymore many households now stretch every dollar just to keep driving. Big car payments paired with steep interest mean trouble hits fast when jobs shrink or bills rise.

4. Used Car Prices Drop Fast

Car values climbed way up during lockdown times. That happened when factories made fewer cars yet people still wanted them badly. Some shoppers paid big amounts, thinking prices would stay that high forever. Yet things changed fast when more vehicles became available again. Buyers started losing interest just as supplies grew larger. Now secondhand car costs are dropping sharply from where they stood before. This swing caused serious money trouble for plenty who borrowed heavily back then.

Used Car Prices Falling:

- Pandemic pricing inflated vehicle costs

- Borrowers now deeply underwater financially

- Falling resale values hurting lenders

- Repossessions increasing market inventory pressure

Lots of people who borrowed money now owe more than what their cars could sell for today. When the car’s value drops below the loan amount, it locks drivers into payments they can’t escape easily. If prices keep climbing and budgets stay tight, making those monthly dues feels heavier especially when the car loses worth faster than expected.

Now worth less, used cars make life harder for those who lend against them. When borrowers fail to pay, selling seized autos brings in smaller sums than before. This gap widens bank losses as missed payments climb higher. A swelling supply of taken-back trucks and sedans might push values down further, one analyst noted. Pressure builds not just on lenders but across the whole secondhand auto world.

5. Inflation Keeps Hurting Workers

Most families still feel the squeeze from rising prices. Essentials like food, medical care, housing, power bills, and child care now take a bigger bite from paychecks far outpacing income gains lately. Working full time does not always mean breathing easier these days. Paying off cars eats into money that once covered basics. Bills pile up where relief should be. For many, what used to stretch across a month barely lasts a few weeks now.

Inflation Pressures on Households Grow:

- Rising costs hurting working families

- Car payments competing with necessities

- Middle-income households facing heavy pressure

- Financial counseling demand steadily increasing

Shelter costs come first for a growing number of people, since power shutoffs hit fast and hard. Car payments might stall not by choice, but due to tight spots where tough picks must be made. When rent and heat demand cash, wheels can wait. Counselors see more families walking in, just trying to shuffle what they owe so they won’t lose rides to work. Buses don’t reach everywhere, after all.

Most people earning a middle wage feel the squeeze help often slips through their fingers, even as bills pile high. Money that once stretched now bends thin, leaving little room when prices climb. Households keep losing hold of what they own, proof these money troubles aren’t rare, but routine.

6. Younger Generations Feel More Pressure

Heavy car bills hit millennials and gen x hardest. Housing eats up big chunks of their paychecks first. Student loans keep piling on stress, then there is kids to raise, day by day getting pricier. On top of that, auto payments stretch budgets even thinner. Getting around while holding down a job means juggling more than ever before.

Younger Borrowers Under Financial Strain:

- Student debt reducing financial flexibility

- Expensive housing limiting household savings

- Vehicle dependence tied to employment

- Economic instability impacting younger generations

Younger adults faced shaky job markets right when they started earning paychecks. Because of recessions and health crises, their early years looked tougher than past decades. Money saved dropped just as prices climbed higher on basics like rent and food. With little set aside, surprise costs now hit harder. When trouble comes, options feel narrow.

Getting around matters most for young people who deliver things, travel far to work, or juggle several jobs at once. Without a working car, money troubles often follow fast. Young adults facing car seizures might struggle later on jobs become harder to keep, building savings gets pushed further out of reach. Some say these setbacks could ripple through their finances for years.

7. Lawmakers Notice

Now drawing scrutiny from Capitol Hill, the rising tide of car seizures puts pressure on regulators to act. Not just activists but also elected officials see trouble in how loan firms handle late payments. Lenders haul away cars fast sometimes too fast sparking debate over what counts as fair play. Under a microscope lately, big-name financing outfits face tough questions from Washington. One probe led by Senator Elizabeth Warren digs into whether people lose their vehicles without proper cause. Speed matters here not recovery of metal and tires, but timing that could cross legal lines.

Government Looks at How Loans Are Given:

- Lawmakers investigating repossession industry practices

- Consumer protections receiving increased attention

- Concerns over aggressive lender actions

- Calls for payment flexibility programs

Borrowers might dodge losing their vehicles if help arrived during tough times options like adjusted due dates or clearer talks with banks could make a difference. Once payments slide, though, certain companies push fast toward taking back cars, say skeptics. A sudden health issue or being out of work shouldn’t mean getting locked out by paperwork done in haste.

Trouble at the state level might push new rules to shield borrowers in car financing down the road. Rising numbers of seized vehicles seem less about poor choices, more about stretched budgets, officials now suggest. With so many struggling to keep a reliable ride, elected leaders are starting to treat this like what it is a widespread problem. Attention from Capitol Hill shows just how deep the strain runs across households nationwide.

8. Personal Stories Show the Human Toll

Lurking beneath each number sits someone’s quiet struggle shaped by tight budgets and sleepless nights. Not wild overspending drives most people here life shocks do, like hospital bills piling up or shifts vanishing overnight. Paychecks shrink while prices climb, nudging regular households toward missed deadlines without clear warning signs. What feels manageable one month slips into crisis the next, draining strength slowly, like water through fingers.

How Losing a Car Affects Feelings:

- Medical emergencies causing payment struggles

- Job losses increasing financial instability

- Transportation loss affecting daily responsibilities

- Emotional stress worsening financial hardship

One moment you’re driving to work, the next you’re stuck on a sidewalk wondering how it fell apart. Losing a car often brings shame, even though money troubles happen to most people at some point. Without wheels, showing up on time turns into a puzzle with missing pieces buses run late, rides fall through. Work feels shaky when your only way there gets taken away. Freedom slips quietly out the door along with the keys.

Long after the repo happens, feelings stick around like smoke in clothes. One surprise bill suddenly years of careful saving unravel. People say it feels like walls closing in, no matter how hard they tried. What looks like data points on a report shows up differently at kitchen tables. A car taken isn’t just metal lost it’s rides to work, school runs, dignity slipping away. Hard times hit unevenly, yet the weight lands heavy every time.

9. The Current Crisis Is Not Like 2008

Right now, folks keep talking about 2008 like it’s happening again but that’s not quite right. Back then, everything fell apart because homes lost value fast, jobs vanished overnight, banks wobbled. This time around, people are losing houses mostly because they can’t afford payments anymore. Not because the whole system is breaking down. A shaky economy isn’t what’s pushing doors open here.

Financial Stress Today Compared to 2008:

- Housing crash not driving crisis

- Inflation gradually squeezing household budgets

- Employment remaining relatively more stable

- Borrowing costs creating affordability problems

These days, joblessness sits much lower than during the 2008 crisis, yet stability in banking doesn’t ease what people feel day to day. Even so, wallets keep tightening under steady inflation and steep loan rates eating into paychecks. Rather than a crash, economists now point to ongoing pressure wearing down family finances across the country piece by piece.

What hits hard isn’t always job loss or market crashes. When prices climb, pay stays flat, trouble builds slowly. Some homes vanish from ownership, not because of collapse, but pressure piling up day by day. Debt grows heavier while room to breathe gets smaller. Stability fades, even when the headlines claim things are fine. Quiet strain spreads through neighborhoods where budgets snap under weight they once held.

10. What Consumers Can Do Moving Forward

Financial experts encourage borrowers facing payment difficulties to contact lenders immediately rather than waiting until repossession becomes unavoidable. Many lenders offer temporary hardship programs, payment extensions, or modified repayment plans for consumers who communicate early enough. Seeking assistance before missing multiple payments can significantly improve the chances of keeping a vehicle.

Strategies for Avoiding Repossession:

- Contact lenders before missing payments

- Explore refinancing or hardship programs

- Seek nonprofit financial counseling assistance

- Consider selling vehicle before default

Some borrowers may benefit from refinancing loans if lower interest rates or longer repayment terms become available. Others may choose to sell their vehicle voluntarily before default occurs in order to minimize long-term financial damage. Financial counselors also recommend carefully reviewing household budgets to identify areas where temporary spending reductions could prevent missed payments.

The growing repossession crisis reflects broader affordability challenges affecting millions of Americans. Vehicles represent far more than transportation because they are directly connected to employment, independence, and family responsibilities. As economic pressures continue building, consumers are being forced to make increasingly difficult financial decisions simply to remain stable and stay on the road.